Still waiting for the right time to invest? The best time was yesterday. The next best time is NOW.

Every day you wait, your money loses value due to inflation. Every month you delay, you miss out on potential gains. Investing isn’t just for the wealthy – it’s for anyone who wants their money to work for them. This guide will show you how to start today, even if you have just RM10.

Why Start Investing Now?

Only 16% of Malaysians invest in the stock market: are you among them, or are you leaving your money to lose value?

84% of Malaysians still rely on savings accounts and fixed deposits, which often fail to keep up with inflation.

Less than 5% invest in ETFs or Robo-Advisors, missing out on easy, passive investment opportunities.

Young Malaysians (aged 18-30) have the biggest advantage >>time<< but many still hesitate due to fear of losses.

Your savings are shrinking. Inflation erodes your money’s purchasing power, meaning RM100 today buys less than RM100 next year.

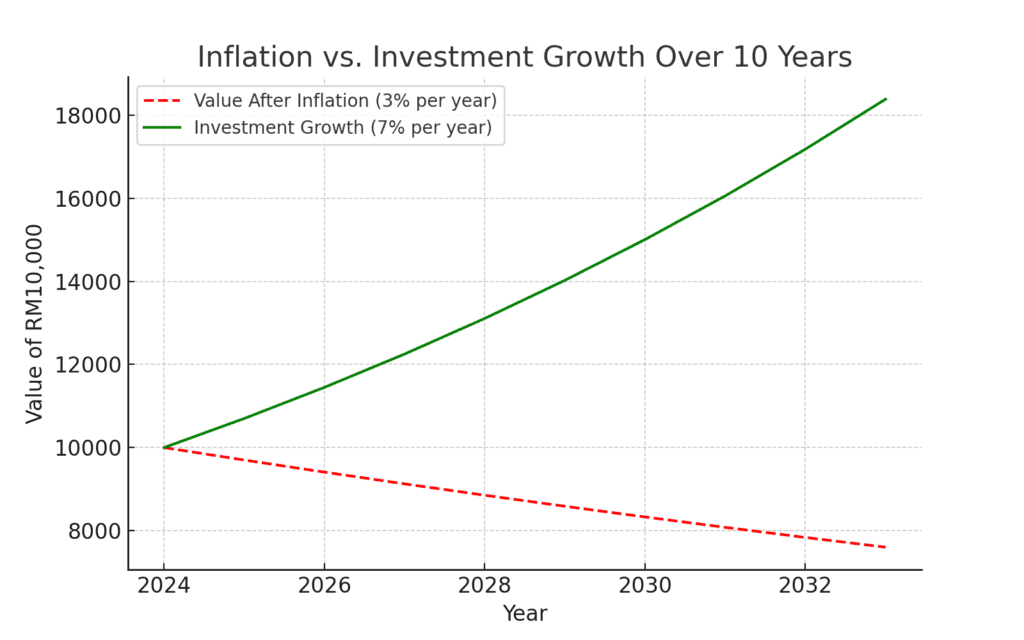

In just 10 years, your RM10,000 loses value due to inflation, while an investment grows nearly double! The longer you wait, the more you lose – start investing now!

Real-Life Example: Waiting vs. Starting Now

Aiman, 25, started investing RM100 per month in a simple Exchange Traded Fund (ETF). His friend, Rizal, waited until he was 35 to start. By the time they turned 50, Aiman had RM150,000 while Rizal had only RM50,000, despite investing the same amount monthly. The only difference? Aiman started earlier.

The biggest mistake? Not starting at all.

Step 1: Define Your Investment Goals

Before investing, ask yourself:

What are you investing for? Retirement, passive income, or financial freedom?

Can you handle short-term losses? Markets fluctuate, but long-term investors win.

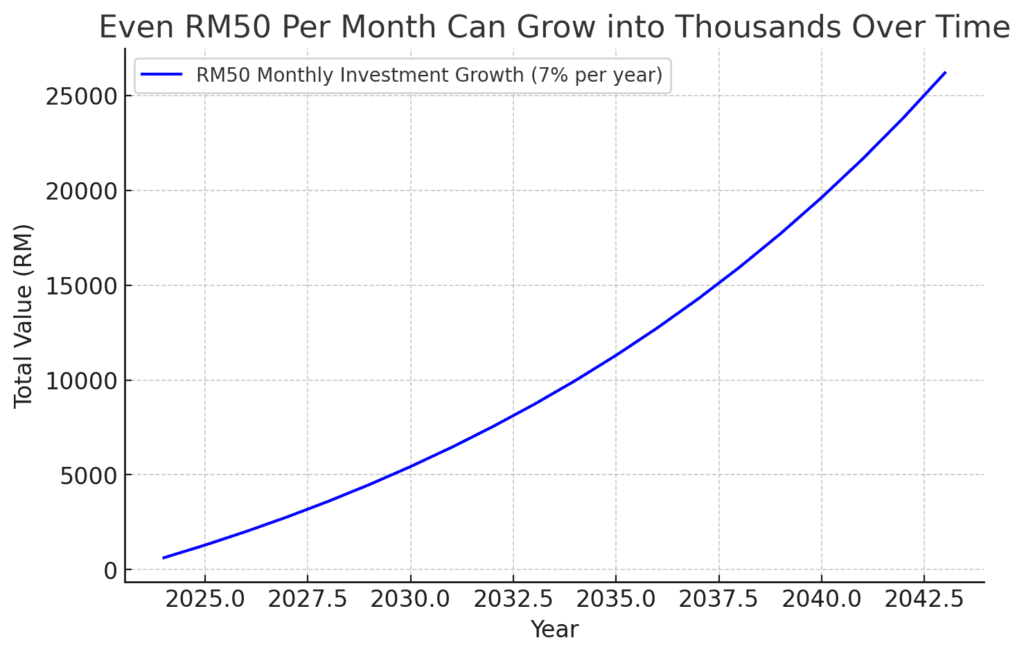

How much can you set aside? Even RM50 per month can grow into thousands over time.

Think RM50 a month won’t make a difference? Think again! This chart shows how a small, consistent investment of RM50 per month can grow into tens of thousands over 20 years – just by letting compound interest do its work

Nudge to Action:

If you don’t define your goals today, when will you? Don’t just think about it, write it down and make it real.

No more waiting. Define your goal today.

Step 2: Overcoming the Fear of Losing Money

One of the biggest reasons people hesitate to invest is the fear of losing money. It’s a valid concern, but here’s the reality:

You only lose money if you sell at the wrong time. Markets go up and down, but history shows that they tend to rise in the long run.

Risk can be managed. The key is diversification, spreading investments across different assets to reduce losses.

Investing is less risky than NOT investing. Inflation erodes the value of cash. Over time, keeping money in a bank account is riskier than investing it wisely.

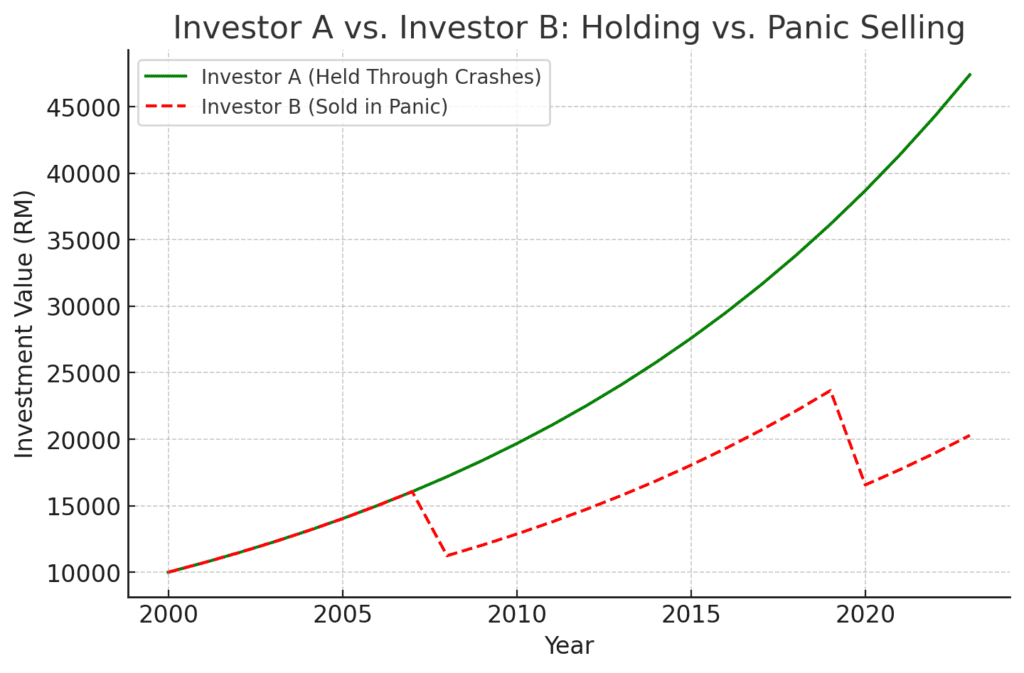

Investor A held through crashes and let their portfolio recover. Investor B sold in panic, locking in losses and missing recovery gains. The difference? Investor A’s portfolio nearly doubled, while Investor B struggled to grow!

How to Reduce Investment Risk

Start small: Begin with RM50 or RM100 per month to gain confidence.

Diversify: Invest in different asset classes like stocks, bonds, and gold.

Use dollar-cost averaging: Invest a fixed amount every month to smooth out market fluctuations.

Think long-term: Avoid panic selling when markets drop.

The real risk isn’t investing – it’s doing nothing and watching your money lose value.

Step 3: Choose Your Investment Type Based on Your Age

Your investment strategy should evolve with age. Here’s where you should focus:

Ages 18-30: Building Aggressive Growth

Stocks & ETFs: High-risk, high-reward investments. Consider blue-chip stocks and index funds.

Robo-Advisors: Automated investing with diversified portfolios.

Cryptocurrency & Alternative Investments: Small allocations for higher returns.

Real Estate Investing (REITs): Good for passive income potential.

Ages 31-45: Balancing Growth and Stability

Diversified Portfolio: Stocks, ETFs, bonds, and unit trusts.

Gold & Precious Metals: Hedge against inflation.

Real Estate Investments: Direct property ownership or REITs.

Fixed Deposits & Bonds: Increasing stability in your investments.

Ages 46-60: Preparing for Retirement

Bonds & Fixed Deposits: Prioritizing capital preservation.

Lower-Risk Mutual Funds: Stability with conservative growth.

Retirement Planning with EPF & PRS: Maximizing savings for post-work life.

Quick Decision Tip:

Not sure where to start? If you want the easiest, low-risk option, begin with Robo-Advisors like StashAway or Wahed Invest. If you’re hands-on, open a Rakuten Trade account and buy your first stock today.

Pick one and commit. No action = no results.

Step 4: Open an Investment Account

To start, you need a brokerage or investment platform. Choose based on what fits your strategy:

5 thoughts on “Most Malaysians Will Retire Broke: Why You Must Start Now Before It’s Too Late (Free Checklist!)”